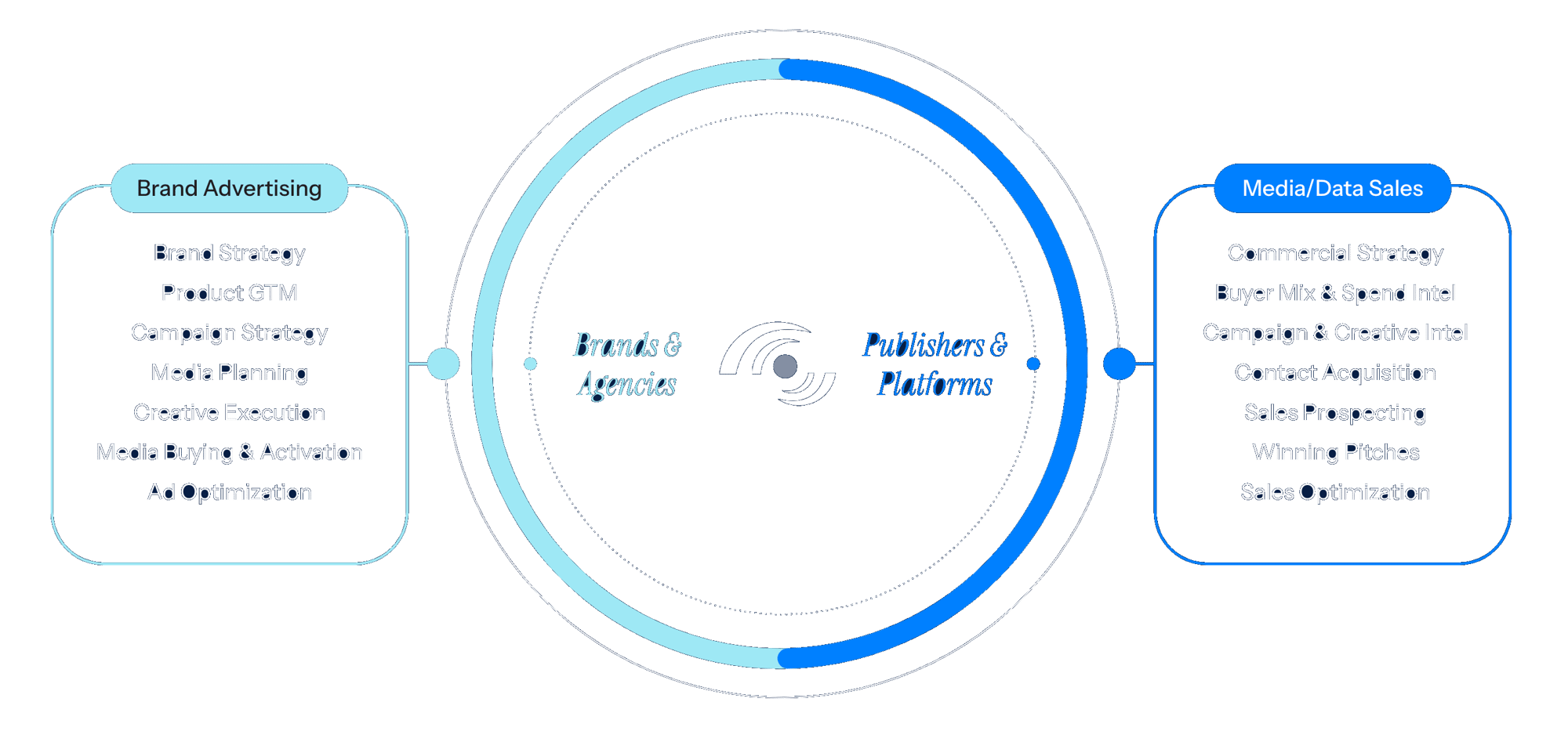

Be a Master of Change

With the largest creative and campaign library in North America at your fingertips, you’re the first to catch every market move. Find new players, track channel growth and place bigger bets with confidence.

Get Money Wise

Follow the money – win your next customer. From assessing your share of wallet to setting targets based on TAM, our media investment insights help you succeed.

Stay Relevant

Trends from millions of creative assets make you an instant creative strategy expert. Engage in the media conversation with ease, no matter where it goes.

MediaRadar provides high-level insights as well as in-depth granularity that you can't get anywhere else. It helps our team sell more effectively.

It is light years ahead...We haven't seen anything like this. Kudos to you for listening to your clients and responding.

MediaRadar paints a clear picture on spend, trends and strategies. The team are problem solvers—they are always available and consistently coming up with solutions to better the product and process.

We work much more efficiently with MediaRadar. From prospecting to trending insights, it's an amazing solution.

.jpeg?width=2000&name=AdobeStock_804293832%20(1).jpeg)

MEDIAWATCH® REPORT

Investment Blueprint 2025: Total Media Report

The MediaWatch Investment Blueprint 2025 is a comprehensive report that provides a roadmap into the media landscape, focusing on media spending trends, strategic approaches by advertisers, and the evolution of both digital and traditional media channels.

REPORT

Future Titans of Pharma & Healthcare Report

This report offers a comprehensive exploration of the pharmaceutical industry's advertising landscape and the standout brands at the forefront. Uncover how these brands are adapting to the changing retail environment.

![]()

.jpg?width=1398&height=783&name=sm_AdobeStock_585413272%20(1).jpg)

REPORT

Future Titans of Retail Report

This focused analysis offers a deep dive into the retail industry, revealing key differences in how retail brands manage their advertising budgets. Discover the strategies that set these brands apart and how they are navigating the evolving retail landscape.

![]()